The Financial Strategy (F3)

Passing CIMA CIMA Strategic exam ensures for the successful candidate a powerful array of professional and personal benefits. The first and the foremost benefit comes with a global recognition that validates your knowledge and skills, making possible your entry into any organization of your choice.

F3 Exam Dumps

- Exam Code: F3

- Vendor: CIMA

- Certifications: CIMA Strategic

- Exam Name: Financial Strategy

Why CertAchieve is Better than Standard F3 Dumps

In 2026, CIMA uses variable topologies. Basic dumps will fail you.

| Quality Standard | Generic Dump Sites | CertAchieve Premium Prep |

|---|---|---|

| Technical Explanation | None (Answer Key Only) | Step-by-Step Expert Rationales |

| Syllabus Coverage | Often Outdated (v1.0) | 2026 Updated (Latest Syllabus) |

| Scenario Mastery | Blind Memorization | Conceptual Logic & Troubleshooting |

| Instructor Access | No Post-Sale Support | 24/7 Professional Help |

Customers Passed Exams

10

Success backed by proven exam prep tools

Questions Came Word for Word

93%

Real exam match rate reported by verified users

Average Score in Real Testing Centre

88%

Consistently high performance across certifications

Study Time Saved With CertAchieve

60%

Efficient prep that reduces study hours significantly

CIMA F3 Exam Domains Q&A

Certified instructors verify every question for 100% accuracy, providing detailed, step-by-step explanations for each.

Question 1

CIMA F3

QUESTION DESCRIPTION:

A company with a market capitalisation of S50million is considering raising $1 million debt to fund a new 10-year capital investment protect

The value of this issue is considered to be small in comparison to the company ' s market capitalisation

The company is considering whether to raise the debt finance by either a " bond private placing ' or a ' public bond issue.

Which THREE of the following statements are correct?

Correct Answer & Rationale:

Answer: A, B, E

Explanation:

CIMA F3 covers takeover defences under Mergers and Acquisitions and Corporate Governance. A crucial distinction is made between legitimate post-offer defences, which are actions taken after a bid has been announced and are consistent with directors’ fiduciary duties, and illegitimate or unethical actions, which may mislead shareholders or breach takeover regulations.

Once a bid is hostile, the directors of the target company (Company B) are required under governance principles emphasised in F3 to act in the best interests of shareholders, not merely to preserve their own positions.

Option A is a legitimate defence.

Having the company’s assets independently and professionally revalued is acceptable and encouraged under CIMA F3. This provides shareholders with objective evidence that the bid undervalues the company and supports informed decision-making without misleading the market.

Option C is a legitimate defence.

Making a counter-bid (often called a “Pac-Man defence”) is permitted provided it can be justified as enhancing shareholder wealth. CIMA F3 stresses that directors may pursue alternative strategic actions if they genuinely believe these will create greater value for shareholders than accepting the hostile offer.

Option E is a legitimate defence.

Referring the bid to competition authorities is allowed where there are genuine competition concerns. CIMA F3 notes that regulatory intervention is an appropriate and lawful route if the acquisition may breach competition law or significantly reduce market competition.

The remaining options are not legitimate:

B is not allowed post-offer, as changing the articles to block a bid breaches takeover rules and shareholder rights.

D is unethical and unlawful, as knowingly publishing misleading forecasts violates disclosure requirements and directors’ duties.

✅ Final Answer: A, C and E

Question 2

CIMA F3

QUESTION DESCRIPTION:

A company plans to raise finance for a new project.

It is considering either the issue of a redeemable cumulative preference share or a Eurobond.

Advise the directors which of the following statements would justify the issue of preference shares over a bond?

Correct Answer & Rationale:

Answer: B

Explanation:

Verified Answer: = B

CIMA F3 compares different forms of long-term finance, including preference shares and bonds/Eurobonds, focusing on control, tax treatment, gearing impact, and flexibility.

Statement B captures a key advantage of preference shares from the company’s perspective: if profits are poor, preference dividends can be omitted or deferred, especially when they are cumulative. Although unpaid dividends accumulate, non-payment does not normally constitute default in the same way as missing an interest payment on a bond. For a Eurobond, failure to pay interest when due would place the company in default, triggering legal and reputational consequences. This extra flexibility is exactly why preference shares might be favoured over bonds.

Statement A is misleading: Eurobonds are often unsecured, and security (or lack of it) is not a defining difference versus preference shares.

Statement C is incorrect in this context: redeemable cumulative preference shares are typically treated as a financial liability under IFRS (like debt), so they would generally increase gearing, not reduce it.

Statement D is clearly wrong as dividends are not tax-deductible, whereas bond interest normally is. Therefore, the best justification for issuing preference shares rather than a Eurobond is B.

Question 3

CIMA F3

QUESTION DESCRIPTION:

An all-equity financed company currently generates total revenue of $50 million.

Its current profit before interest and taxation (PBIT) is $10 million.

Due to difficult trading conditions, the company expects its total revenue to be constant next year, although some margins will reduce.

It forecasts next year ' s PBIT will fall to 18% on 40% of its revenue, but that the PBIT on the other 60% of its revenue will be unaffected.

The rate of corporate tax is 20%.

What is the forecast percentage reduction in next year ' s Earnings?

Correct Answer & Rationale:

Answer: C

Explanation:

Current year:

Revenue = $50m

PBIT = $10m → margin = 10/50 = 20%

Tax = 20%

Earnings = 10 × (1 − 0.20) = $8m

Next year:

Revenue still $50m

40% of revenue = $20m → margin falls to 18%

PBIT on this part=20×18%=3.6\text{PBIT on this part} = 20 \times 18\% = 3.6PBIT on this part=20×18%=3.6

60% of revenue = $30m → margin stays 20%

PBIT on this part=30×20%=6.0\text{PBIT on this part} = 30 \times 20\% = 6.0PBIT on this part=30×20%=6.0

Total PBIT next year:

3.6+6.0=9.6 million3.6 + 6.0 = 9.6\ \text{million}3.6+6.0=9.6 million

Earnings after tax next year:

9.6×(1−0.20)=9.6×0.8=7.68 million9.6 \times (1 - 0.20) = 9.6 \times 0.8 = 7.68\ \text{million}9.6×(1−0.20)=9.6×0.8=7.68 million

Percentage reduction in earnings:

8.00−7.688.00=0.328=0.04=4%\frac{8.00 - 7.68}{8.00} = \frac{0.32}{8} = 0.04 = 4\%8.008.00−7.68=80.32=0.04=4%

Correct option:

C. Reduction of 4.0%\boxed{\text{C. Reduction of 4.0\%}}C. Reduction of 4.0%

Question 4

CIMA F3

QUESTION DESCRIPTION:

Company GDD plans to acquire Company HGG, an unlisted company which has been in business for 3 years.

Company HGG has incurred losses in its first 3 years but is expected to become highly profitable in the near future

There are no listed companies in the country operating in the same business field as Company HGG The future success of Company HGG ' s business and hence the future growth rate in earnings and dividends is difficult to determine

Company GDD is assessing the validity of using the dividend growth method to value Company HGG

Which THREE of the following are weaknesses of using the dividend growth model to value an unlisted company such as Company HGG?

Correct Answer & Rationale:

Answer: A, C, E

Explanation:

Company HGG is young, unlisted, loss-making so far, and has uncertain growth.

Weaknesses of using the dividend growth model here:

A. Future growth rate in earnings/dividends is hard to estimate – very true for an early-stage, high-uncertainty business.

C. It has been unprofitable and has no established dividend pattern, so the basic inputs to the model (D₀ and g) are unreliable.

E. Cost of capital is difficult to estimate for an unlisted company (no directly observable beta or market data).

B is just a description of the model, not a specific weakness here, and D is incorrect because the dividend growth model does discount future dividends (it fully incorporates time value of money).

✅ Answer Q121: A, C, E

Question 5

CIMA F3

QUESTION DESCRIPTION:

Company RRR is a well-established, unlisted, road freight company.

In recent years RRR has come under pressure to improve its customer service and has had some success in doing this However, the cost of improved service levels has resulted in it making small losses in its latest financial year. This is the first time RRR has not been profitable.

RRR uses a ' residual ' dividend policy and has paid dividends twice in the last 10 years.

Which of the following methods would be most appropriate for valuing RRR?

Correct Answer & Rationale:

Answer: A

Explanation:

Most appropriate is asset-based valuation because RRR is unlisted, has just made a loss and pays dividends only occasionally. Earnings- and dividend-based models (P/E, earnings yield, DVM) rely on stable, positive earnings or dividends, which RRR does not currently have, so valuing the tangible and identifiable intangible assets is more reliable.

Question 6

CIMA F3

QUESTION DESCRIPTION:

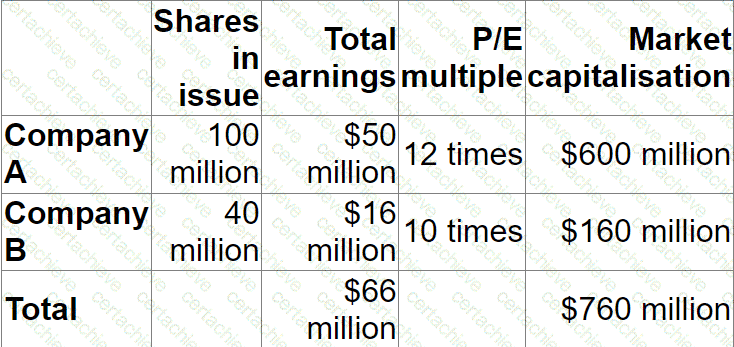

Company A plans to acquire Company B in a 1-for-1 share exchange.

Pre-acquisition information is as follows:

Post-acquisition information is as follows:

Annual earnings are expected to increase by $4 million.

The P/E multiple of the combined company is expected to be 12 times.

If the acquisition proceeds, what is the expected percentage increase in the post acquisition share price of Company A?

Correct Answer & Rationale:

Answer: D

Explanation:

Pre-acquisition

Company A

Earnings = $50m

P/E = 12 → Market value = 50 × 12 = $600m

Shares = 100m → Share price = 600 / 100 = $6.00

Company B

Earnings = $16m

Combined current earnings = 50 + 16 = $66m.

Post-acquisition assumptions

Earnings increase by $4m → New total earnings

= 66 + 4 = $70m

Combined P/E = 12

→ Total market value = 70 × 12 = $840m

Effect of the 1-for-1 share exchange

Company B has 40m shares, so Company A issues 40m new shares.

New total shares in Company A = 100m + 40m = 140m

Post-acquisition share price:

New price=Total valueTotal shares=840m140m=$6.00\text{New price} = \frac{\text{Total value}}{\text{Total shares}} = \frac{840m}{140m} = \$6.00New price=Total sharesTotal value=140m840m=$6.00

This is the same as the original $6.00, so the percentage increase in Company A’s share price is:

6.00−6.006.00=0%\frac{6.00 - 6.00}{6.00} = 0\%6.006.00−6.00=0%

So the expected increase in share price is 0%.

Question 7

CIMA F3

QUESTION DESCRIPTION:

Which THREE of the following statements are correct in respect of the issuance of debt securities.

Correct Answer & Rationale:

Answer: A, B, E

Explanation:

A. “A bond issuer must appoint at least one market-maker…” – TRUE (in exam context)

On public bond markets, an issuer typically works with one or more banks/dealers as market-makers. Their role is to quote buy and sell prices and help ensure liquidity so investors can trade in and out. From an exam perspective, this is treated as a standard feature of traded corporate/government bonds.

B. “The redemption yield… can be determined by calculating the internal rate of return…” – TRUE

The redemption yield (yield to maturity) is exactly the IRR of the bond’s cash flows (all coupon payments plus redemption amount) based on the current market price. That’s standard CIMA F3 territory.

C. “Investors in traded bonds have an ownership stake…” – FALSE

Bondholders are creditors, not owners. They have a contractual right to interest and principal, but no equity participation, voting rights, or residual claim (except in liquidation after other priorities).

D. “A first-time bond issuer will find it easier to issue bonds than arrange a conventional term loan.” – FALSE

It’s usually the opposite. For a new issuer, arranging a bank term loan is typically quicker and simpler than accessing the bond market, which involves credit ratings, documentation, listing and investor marketing.

E. “Governments are the most frequent issuers of bonds…” – TRUE

Governments regularly issue sovereign bonds (treasuries, gilts, etc.) both to finance spending and to roll over existing national debt. This is exactly how public deficits are funded in practice and is a standard statement in financial strategy texts.

Hence: A, B and E.

Question 8

CIMA F3

QUESTION DESCRIPTION:

A company ' s current profit before interest and taxation is $1.1 million and it is expected to remain constant for the foreseeable future.

The company has 4 million shares in issue on which the earnings yield is currently 10%. It also has a $2 million bond in issue with a fixed interest rate of 5%.

The corporate income tax rate is 20% and is expected to remain unchanged.

Which of the following is the best estimate of the current share price?

Correct Answer & Rationale:

Answer: C

Explanation:

PBIT = $1.1m

Debt = $2m at 5% → interest = $0.1m

Profit before tax = 1.1 – 0.1 = $1.0m

Tax at 20% = 0.2m → Earnings after tax = $0.8m

Earnings yield = Earnings ÷ Market value of equity = 10%:

0.8=0.10×MV⇒MV=0.80.10=$8m0.8 = 0.10 \times \text{MV} \Rightarrow \text{MV} = \frac{0.8}{0.10} = \$8\text{m}0.8=0.10×MV⇒MV=0.100.8=$8m

Shares in issue = 4m → share price:

Price=84=$2.00\text{Price} = \frac{8}{4} = \$2.00Price=48=$2.00

Answer: C: $2.00

Question 9

CIMA F3

QUESTION DESCRIPTION:

A listed company in the retail sector has accumulated excess cash.

In recent years, it has experienced uncertainly with forecasting the required level of cash for capital expenditure due to unpredictable economic cycles.

Its excess cash is on deposit earning negligible returns.

The Board of Directors is considering the company ' s dividend policy, and the need to retain cash in the company.

Which THREE of the following are advantages of retaining excess cash in the company?

Correct Answer & Rationale:

Answer: C, D, E

Explanation:

C – More cash = able to react quickly to unexpected investment opportunities.

D – Cash buffer reduces the likelihood of liquidity problems in a downturn.

E – If excess cash were returned, markets might read it as “no good growth opportunities”, so retaining avoids that negative signal.

Question 10

CIMA F3

QUESTION DESCRIPTION:

Which THREE of the following statements are disadvantages of the net asset basis of valuation?

Correct Answer & Rationale:

Answer: B, D, E

Explanation:

Disadvantages of net asset basis:

B – Net book value is historic cost based and reflects accounting conventions, not current value.

D – Net realisable value is usually different from NBV, so NBV may misstate value.

E – Many intangible assets (brands, goodwill, know-how) are missing from the balance sheet, so value is understated.

Answer (Q116): B, D, E

Verified by Certified Instructors

This CIMA F3 study pack was audited and verified on August 9, 2026 by Aswath Sinclair,. We ensure every technical rationale aligns with real-world enterprise standards.

A Stepping Stone for Enhanced Career Opportunities

Your profile having CIMA Strategic certification significantly enhances your credibility and marketability in all corners of the world. The best part is that your formal recognition pays you in terms of tangible career advancement. It helps you perform your desired job roles accompanied by a substantial increase in your regular income. Beyond the resume, your expertise imparts you confidence to act as a dependable professional to solve real-world business challenges.

Your success in CIMA F3 certification exam makes your visible and relevant in the fast-evolving tech landscape. It proves a lifelong investment in your career that give you not only a competitive advantage over your non-certified peers but also makes you eligible for a further relevant exams in your domain.

What You Need to Ace CIMA Exam F3

Achieving success in the F3 CIMA exam requires a blending of clear understanding of all the exam topics, practical skills, and practice of the actual format. There's no room for cramming information, memorizing facts or dependence on a few significant exam topics. It means your readiness for exam needs you develop a comprehensive grasp on the syllabus that includes theoretical as well as practical command.

Here is a comprehensive strategy layout to secure peak performance in F3 certification exam:

- Develop a rock-solid theoretical clarity of the exam topics

- Begin with easier and more familiar topics of the exam syllabus

- Make sure your command on the fundamental concepts

- Focus your attention to understand why that matters

- Ensure hands-on practice as the exam tests your ability to apply knowledge

- Develop a study routine managing time because it can be a major time-sink if you are slow

- Find out a comprehensive and streamlined study resource for your help

Ensuring Outstanding Results in Exam F3!

In the backdrop of the above prep strategy for F3 CIMA exam, your primary need is to find out a comprehensive study resource. It could otherwise be a daunting task to achieve exam success. The most important factor that must be kep in mind is make sure your reliance on a one particular resource instead of depending on multiple sources. It should be an all-inclusive resource that ensures conceptual explanations, hands-on practical exercises, and realistic assessment tools.

Certachieve: A Reliable All-inclusive Study Resource

Certachieve offers multiple study tools to do thorough and rewarding F3 exam prep. Here's an overview of Certachieve's toolkit:

CIMA F3 PDF Study Guide

This premium guide contains a number of CIMA F3 exam questions and answers that give you a full coverage of the exam syllabus in easy language. The information provided efficiently guides the candidate's focus to the most critical topics. The supportive explanations and examples build both the knowledge and the practical confidence of the exam candidates required to confidently pass the exam. The demo of CIMA F3 study guide pdf free download is also available to examine the contents and quality of the study material.

CIMA F3 Practice Exams

Practicing the exam F3 questions is one of the essential requirements of your exam preparation. To help you with this important task, Certachieve introduces CIMA F3 Testing Engine to simulate multiple real exam-like tests. They are of enormous value for developing your grasp and understanding your strengths and weaknesses in exam preparation and make up deficiencies in time.

These comprehensive materials are engineered to streamline your preparation process, providing a direct and efficient path to mastering the exam's requirements.

CIMA F3 exam dumps

These realistic dumps include the most significant questions that may be the part of your upcoming exam. Learning F3 exam dumps can increase not only your chances of success but can also award you an outstanding score.

Top Exams & Certification Providers

New & Trending

- New Released Exams

- Related Exam

- Hot Vendor